A Long, Hard Road—Nebraska State Legislative Tax Update

Nebraska’s 2023 Legislative Session—Slow Going

The 2023 Nebraska Unicameral Legislative Session attracted national attention on more than one occasion due to controversial bills, debates, and comments from senators. One senator’s statement that she would “burn the session to the ground”[1] over a controversial bill foretold of difficulties to come.

Though not as provocative as guns or abortion, LB 206, which was rolled into LB 754, is a tax bill that will significantly affect tax preparers’ discussions with their pass-through entity clients.

PTETs and “SALT Workarounds”—In General

The federal legislation known as the Tax Cuts and Jobs Act (“TCJA”) passed in 2017, limiting the federal income tax deduction for state and local taxes for individuals to $10,000. The TCJA thus had a potentially negative impact on individual owners of pass-through entities, such as S corporations or partnerships.

As a result, many states implemented “pass through entity tax” (“PTET”) elections to shift the tax burden from the individual to the entity,[2] allowing the partnership to take the full deduction.

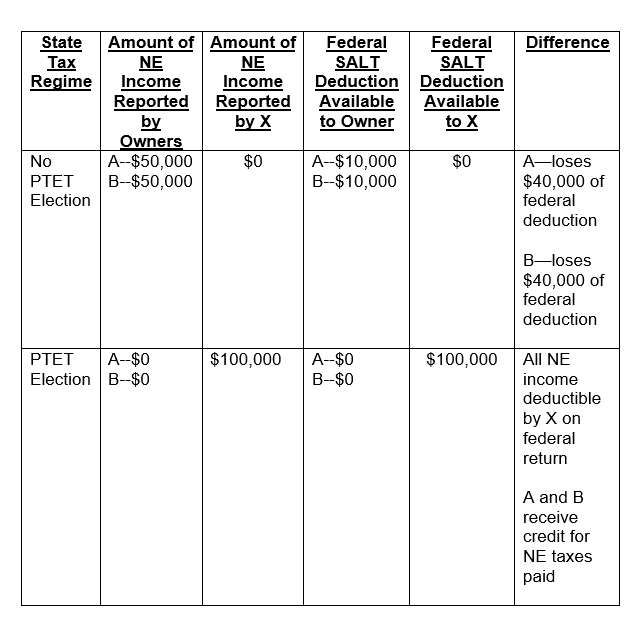

PTET elections vary by state. Generally, the partnership or entity pays the state income tax and then the entity claims the state income tax payment as a deduction on the entity’s federal tax return. This, in turn, decreases the income reported on the partner’s K-1 and the partner’s federal income tax return. Most states require the partner to add-back the state taxes deducted from federal income.[3] States generally allow the partner to then claim a credit for the share of PTET or will allow the partner to exclude the previously taxed income.[4] The following simple Example illustrates how a PTET election works:

Example—PTET Election

Assume A and B each own a 50% equity interest in a flow-through entity (“X”), and that A and B equally share in the tax allocations from X. Also assume that for the tax year in question, X has total Nebraska income of $100,000

Proposed Nebraska PTET Election

On February 23, 2023, Senator Lou Ann Linehan, by way of an amendment to LB 206, proposed a PTET election for Nebraska. LB 206, later rolled into LB 754, in conjunction with the Linehan amendment, permits eligible “small business corporations”[5] and “eligible partnerships”[6] to make an annual, irrevocable election to pay the taxes, interest, or penalties levied by the Nebraska Revenue Act of 1967 at the entity level for the taxable period covered by the return.[7]

In practice, the partners of an eligible partnership and shareholders of an eligible S corporation would still need to file a Nebraska return to report their pro rata or distributive share of the income of the partnership or S corporation, as applicable. The partnership or S corporation would add back any amount of Nebraska tax imposed under the Nebraska Revenue Act of 1967 and deducted by the entity for federal income tax purposes. Notably, any nonresident individual who is an owner of an electing entity would not be required to file a Nebraska tax return if the only source of income connected with Nebraska is from an electing entity and if such nonresident’s individual tax would be satisfied by the credit.[8]

There remain unanswered questions and considerations. The NDOR has not released forms to make the election. Additionally, the process for obtaining the election is not outlined in the bill.

Special Election for Partnerships Filing Amended Returns

If an entity taxed as a partnership is filing an amended Form 1065N that results in additional Nebraska income tax, LB 754 also allows the partnership to pay the tax, penalties, and interest on behalf of its partners for the years in question.[9] A separate election would presumably be required for this special provision, and tax would be paid by the partnership at the highest individual income tax rate.[10] This election would allow partnerships to choose whether or not to pay additional tax relating to an amended return, without the need for partners to pay the tax, penalties, and interest in a manner similar to the federal partnership audit rules.[11] Electing partnerships would not be required to send out Form K-1Ns to each partner, which could be convenient for partnerships.[12]

Implications for Preparers

LB 754 creates opportunities for preparers to maximize the federal SALT deduction available for eligible partnerships and S corporations. LB 754 allows preparers to make retroactive PTET elections for tax years beginning on or after January 1, 2018.[13] However, whether an election is appropriate depends on a number of factors, including the following:

- Whether the eligible partnership or S corporation had operating losses for the tax year in question.

- The number of owners of the eligible entity, and the resulting hassle of amending federal returns and filing for federal refunds.

- The complexity involved with tiered pass-through entities.

- Whether the eligible entity has sufficient available cash to pay the Nebraska income tax.

Questions may also arise about whether or not owners of an eligible entity should withhold estimated Nebraska income taxes going forward. Likewise, adjustments to federal estimated payments may be required considering the availability of an increased federal SALT deduction.

If you have questions regarding how the PTET election may affect your business, please contact a Baird Holm LLP attorney.

[1] See Associated Press, A Nebraska Legislator is 3 Weeks into a Filibuster over a Trans Bill, NBC News (Mar. 15, 2023, 10:01 AM) https://www.nbcnews.com/nbc-out/out-politics-and-policy/nebraska-lawmaker-3-weeks-filibuster-trans-bill-rcna75043.

[2]See States with Enacted or Proposed Pass-Through Entity (PTE) Level Tax (Apr. 21, 2023) https://us.aicpa.org/content/dam/aicpa/advocacy/tax/downloadabledocuments/56175896-pte-map.pdf. This resource includes a list of states with enacted or proposed PTET. Note, Connecticut’s pass-through entity tax is mandatory whereas other states make it optional. Nebraska is one of seven (7) states that have not yet passed a PTET election option.

[3] See Russ Smith, Tax Consulting Director, A Guide on State Pass-Through Entity Tax Elections (PTET), LUTZ (Jan. 26, 2023), https://www.lutz.us/blog/comprehensive-guide-pass-through-entity-tax-elections#:~:text=The%20benefit%20of%20the%20PTET,known%20as%20the%20SALT%20cap.

[4] See id.

[5] An eligible small business corporation is defined as an entity subject to taxation under subchapter S of the Internal Revenue Code.

[6] “Partnerships” would include any entity taxable as a partnership for federal income tax purposes, including LLCs, LPs, LLPs, and GPs but excludes “publicly traded partnerships.”

[7] See LB206 AM556 (6)(a) and (8)(a), https://www.nebraskalegislature.gov/FloorDocs/108/PDF/AM/AM556.pdf.

[8] https://www.nebraskalegislature.gov/FloorDocs/108/PDF/AM/AM556.pdf.

[9] See LB206, Section 4.

[10] See Revenue Committee Statement, https://nebraskalegislature.gov/FloorDocs/108/PDF/CS/LB206.pdf.

[11] See Introducer’s Statement of Intent, https://nebraskalegislature.gov/FloorDocs/108/PDF/SI/LB206.pdf. See also Fed. Reg. 27334, https://www.govinfo.gov/content/pkg/FR-2017-06-14/pdf/2017-12308.pdf.

[12] See Introducer’s Statement of Intent, https://nebraskalegislature.gov/FloorDocs/108/PDF/SI/LB206.pdf.

[13] See LB206 AM556 (6)(a), https://nebraskalegislature.gov/FloorDocs/108/PDF/AM/AM556.pdf.